Property Refurbishment Finance

For small and medium scale renovations, refurbishments, and conversions

Property Refurbishment Finance

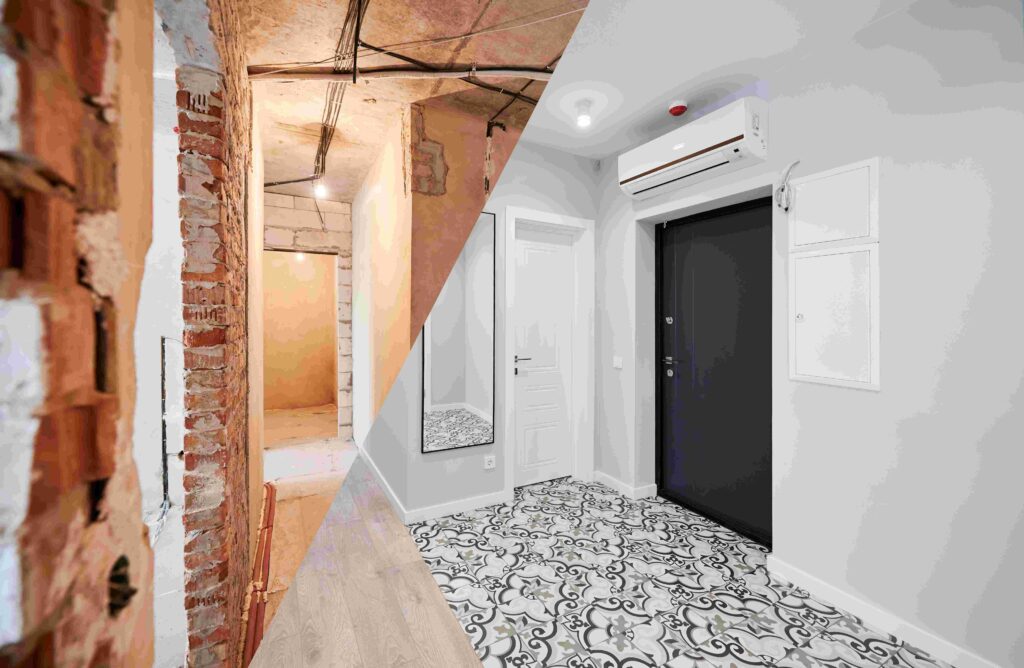

Property Refurbishment Finance encompasses a range of loan products designed to support smaller-scale renovation projects, distinct from the larger-scale projects typically suited to Property Development Finance. These products are ideally suited for residential properties requiring minor refurbishments, scaling up to and including upgrades to plumbing, heating, and electrical systems, as well as window and door replacements, and complete facelifts. This finance option also caters to conversions, such as transforming larger residences into Houses in Multiple Occupation (HMOs). The available range includes separate bridging loans, which are then replaced by long-term finance if the property is to be retained. Some arrangements involve a bridge loan and a long-term buy-to-let loan agreed upon at the outset, with the product switch occurring swiftly once the building work is completed. Additionally, there are single long-term buy-to-let loans available, incorporating a period at the start of the loan for building work completion. Borrowers of Property Refurbishment Finance can expect features like staged funding, adaptable repayment terms, and potentially interest roll-up facilities, with each lender tailoring their offerings to the unique needs of these smaller yet impactful projects. Below, we offer essential information covering principal considerations and critical factors regarding Property Refurbishment Finance, intended for your review before initiating the application process with us.

YOUR PROJECT, OUR MISSION

Supporting UK businesses with access to Finance That Fits

Product Types

For larger-scale projects traditional Property Development Finance is often the most appropriate choice. In certain cases, depending on the range of assets in the borrower’s property portfolio, raising capital against a property not directly involved in the project can also be an option worth consideration, but there are solutions tailored to small and medium sized refurbishment projects, and the following product are often a good fit.

Bridge Finance:

Bridge finance is a pivotal solution in several scenarios, including the acquisition of properties and raising funds for refurbishment work. It’s particularly beneficial when a long-term finance option, like a buy-to-let mortgage, is not suitable due to various reasons such as the nature of the property or the urgency of the purchase. This form of finance is advantageous when:

Purchasing a Property: It enables quick acquisition, especially when the property in question is not eligible for standard long-term mortgages due to its condition or other factors.

Existing Property Constraints: For properties already owned, particularly those with existing mortgages that restrict vacating or refurbishing, bridge finance offers a flexible solution.

Unencumbered Properties: In cases where a property is unencumbered, bridge finance can be a strategic choice to raise funds for refurbishment.

For more detailed information on bridge finance, please visit our dedicated Bridge Finance page.

Dual-Phase Finance:

Dual-Phase Finance is an increasingly popular product, which can be an excellent choice to achieve a higher degree of certainty on day 1, whilst retaining the flexibility associated with Bridge Finance during the refurbishment phase. This product combines two distinct loans:

Initial Bridge Loan: At the project’s inception, a bridge loan is provided. This facilitates immediate funding needs, whether for acquisition or the commencement of refurbishment work.

Transition to Buy-to-Let Mortgage: Pre-agreed with the same lender, this finance transforms into a long-term buy-to-let mortgage upon completion of the refurbishment. This seamless transition provides a structured path from development to rental.

This dual-phase approach offers clarity and continuity, ensuring predictability throughout the project lifecycle.

Refurbishment Buy-to-Let Mortgage:

An example of a more tailored solution is the ‘Refurbishment Buy-to-Let Mortgage’:

Long-Term Mortgage with Refurbishment Provision: This mortgage type is agreed upon for the long term but uniquely allows for refurbishment work to be carried out in its initial period, typically up to three months.

Funding Scope: Suitable for a range of refurbishments, from minor cosmetic updates to more substantial modernization efforts.

Financial Flexibility: It provides a blend of immediate refurbishment funding coupled with the stability of a long-term rental mortgage.

This product is especially beneficial for borrowers seeking a single, comprehensive financial solution for both refurbishing and then renting out a property.

Loan to Value (LTV)

Loan to Value (LTV) is a critical factor to consider in Property Refurbishment Finance. The post-refurbishment plans, whether involving retaining the property long-term and letting it out, or selling it, will have a crucial influence, among other factors, on planning the correct financing solution or solutions.

Bridge Finance: In bridge finance, the maximum achievable loan size initially is closely tied to the property’s current value. LTV considerations are crucial, especially when factoring in the potential to roll up interest. This type of finance is less concerned with ongoing rental income for serviceability and focuses more on LTV, taking into account the loan amount provided and any rolled-up interest, measured against the property’s value. A prime example of when bridge finance may be the right option is when the maximum loan amount is required upfront, particularly if the property is intended to be sold after refurbishment, or when other funds are expected to be received soon, thereby reducing the overall debt levels required.

Dual-Phase Finance and Refurbishment Buy-to-Let Mortgage: With products like Dual-Phase Finance and Refurbishment Buy-to-Let Mortgages, the initial loan amount is often capped by the lower of the maximum LTV acceptable to the lender or the property’s predicted market rent value post-refurbishment. This approach ensures that the rental income post-refurbishment is adequate to service the long-term loan established at the beginning, preventing the loan amount from exceeding a level that would make the post-refurbishment rental income insufficient for regular loan repayments.

It’s imperative to tailor the choice of product or combination of products from the outset to align with the borrower’s plans for the property, whether that involves retaining and renting it out, or selling it. Such strategic planning is key to ensuring that the loan structure matches the borrower’s long-term property goals and financial situation. This is one of the many ways in which Fit To Lend can assist you and add value.

Eligibility and Requirements

Property Refurbishment Finance offers a spectrum of loan products, each tailored to specific types of renovation projects and borrower needs. The eligibility and requirements for these loans vary significantly, depending on the specific product type and project characteristics. It’s important that we understand your circumstances properly so that we can recommend the best solution.

The Project: For more straightforward projects, such as basic refurbishments on average-sized properties, while lenders typically want details of the project plans, prior experience may not be a strict requirement. However, for more challenging projects involving extensive building work or higher-risk property types, lenders may place greater emphasis on the borrower’s previous experience and require more detailed plans.

Financial: The financial requirements for property refurbishment finance also differ based on the loan product. In the case of bridging loans, the primary consideration is often ensuring that the Loan-to-Value (LTV) is always maintained at an acceptable level and that the exit strategy or strategies are credible. More bespoke refurbishment products might require borrowers to demonstrate additional financial reserves, for example, to cover interest payments and the cost of works during the period when the building work is being completed and before the property is ready for occupation or letting. Where the property is to be retained and future rents will service loan payments, the lender will assess affordability based on the valuers opinion of Market Rent Value.

The Timetable: The timeframe allowed for the completion of refurbishment work is another variable factor and is highly dependent on the specific loan product chosen. Borrowers with less certain project timelines might find bridge finance more accommodating due to its inherent flexibility.

The Borrower: In terms of borrower eligibility, property refurbishment finance is available to a wide range of entities, including sole traders, limited companies, and partnerships. Most product options are accessible to these business types. Borrowers with or without experience can apply dependent on the project characteristics, and subject to the particular lenders criteria. While the age of borrowers can be a consideration in some scenarios, it usually does not pose an insurmountable barrier. However, in situations where age is a factor, it’s crucial to carefully consider the most appropriate lenders and product structures.

Each product option’s criteria are designed to cater to the specific demands and risks associated with different types of refurbishment projects. Matching your requirements to the right product is essential, and it can be tricky, but don’t worry – we’re here to help

Interest rates & fees

The pricing of Property Refurbishment Finance will depend on the specific financing product or products used, as interest rates and fees can vary significantly.

Bridge Finance: When opting for bridge finance as a standalone option, interest rates and fees are governed by the norms of bridging loans. These rates are subject to the specifics of the bridge finance agreement. For more detailed information on these rates, please refer to our Bridge Finance webpage.

Dual-Phase Finance: In arrangements that combine a bridge loan with a long-term buy-to-let mortgage (dual-phase finance), pricing is typically agreed upon at the outset. This consolidated approach can offer potential savings, as the rates and fees for both phases of financing are established simultaneously from day one with the same lender.

Refurbishment Buy-to-Let Mortgage: For projects financed through a refurbishment buy-to-let mortgage, providing a single facility from the start, this option can provide the most cost-effective solution, possibly accompanied by some stricter criteria and reduced flexibility. This approach can be particularly cost-effective for borrowers intending to retain the property after refurbishment.”

The application, approval, and completion processes

The application process for Property Refurbishment Finance involves careful preparation and presentation of the required documentation. At Fit to Lend, we offer comprehensive support throughout this journey, beginning with an assessment of the borrower’s circumstances, needs, and refurbishment plans. We specialize in identifying the most suitable refurbishment finance product, ensuring it aligns with the borrower’s project objectives.

Our role extends beyond mere facilitation; we strive to craft a credible and compelling proposal to enhance the likelihood of lender approval for your refurbishment project. By remaining actively involved at every stage—liaising with borrowers, lenders, valuers, and solicitors—we navigate the complexities of the process to meet your project timeline. Our commitment is to ensure that from initial application to final completion, every step of your property refurbishment finance is handled with diligence and expertise, minimizing delays and aligning with your project goals.

working with lenders, for borrowers

Supporting UK businesses with access to Finance That Fits

Other Finance Solutions

questions

&

Answers

Yes, we charge a transparent and fair fee of 0.5% that's typically payable at the end when the loan completes, and in our opinion borrowers should be extra cautious if a broker ever offers to work without charging a fee. In these circumstances the broker's income may be based solely on commissions paid by lenders, and commissions vary significantly between different lenders, so the borrower needs to be confident that the broker is not inappropriately influenced by lender commissions. It is critically important that the broker has the borrowers best interests front & centre when presenting choices and making recommendations. Our fee is modest, and if you take a look at what it represents as a portion of borrowing costs over the loan term, you'll see why we're confident it will be far outweighed by the savings we achieve for borrowers and the value of the close support and guidance we provide.

LTV is based on current property value, loan amount, and potential interest roll-up. The post refurbishment value may also be estimated and a further advance of the loan made available once building work has been completed and the property let.

make

an

enquiry

News, Views And Finance Clues

working with lenders, for borrowers

Supporting UK businesses with access to Finance That Fits

Other Commercial Finance Solutions

More News, Views And Finance Clues

EXPERT EVALUATION, EFFECTIVE EXECUTION

Supporting UK businesses with access to Finance That Fits